The Zillow Consumer Housing Trends Report 2023* seems to think you are willing to try something new ...

In 2023, 95% of buyers used at least one online source in the home shopping process ...

84% using a mobile device

89% of buyers reported using at least one digital home shopping tool,

and 53% reported that they signed paperwork digitally

29% found their mortgage lender from a referral (agent, friend, family),

but 33% found them from online sources

And the #1 item that buyers want in a home for the fifth year in a row ...

84% want a home to fit their initial budget

* https://www.zillow.com/research/buyers-housing-trends-report-2023-32978/

The interesting thing about the last item (84% wanting their home to fit their initial budget) ... with home prices and interest rates having trended upwards for the last three years, we are seeing many buyers step aside.

With home-ownership being the single biggest asset class that leads to multi-generational wealth-building for all households in the United States, this is unfortunate.

Having been a residential lender for 38 years and having been married to a Realtor for 40 years, seeing prospective home-buyers being forced to choose to pay countless thousands of dollars toward rents, year after year, enriching landlords instead of their families/households is frustrating.

So I have a new tool for you to check out ... a new company named HomeBuck$

With home-ownership being the single biggest asset class that leads to multi-generational wealth-building for all households in the United States, this is unfortunate.

Having been a residential lender for 38 years and having been married to a Realtor for 40 years, seeing prospective home-buyers being forced to choose to pay countless thousands of dollars toward rents, year after year, enriching landlords instead of their families/households is frustrating.

So I have a new tool for you to check out ... a new company named HomeBuck$

Powered by a "whole house" based mortgage optimization software program I have been developing over the past 15 years, named "TCO®-flex, HomeBuck$ will show prospective home-buyers (like you) how to significantly reduce the total cost of owning their new homes (in periods of high interest rates or low interest rates).

So how does it all work? ... well, the first thing you need to figure out is that I am a hard core math guy. When I talk to one of my clients about financing their new home ... using the TCO®-flex software, I have the ability to look at upwards of 32 billion different structures for the financial side of owning their home to see which one they like best (this takes about one minute). Thirty-two Billion is a bunch, so showing you how it all works would be very difficult, especially since each client is different and each prospective home is different. So, the best way to show you what HomesBuck$ is all about is to share with you a recent financial model I developed for a new listed property represented by Ginny Nevins - Broker/Owner of Windsor Realty, in Berkeley Lake, Ga.

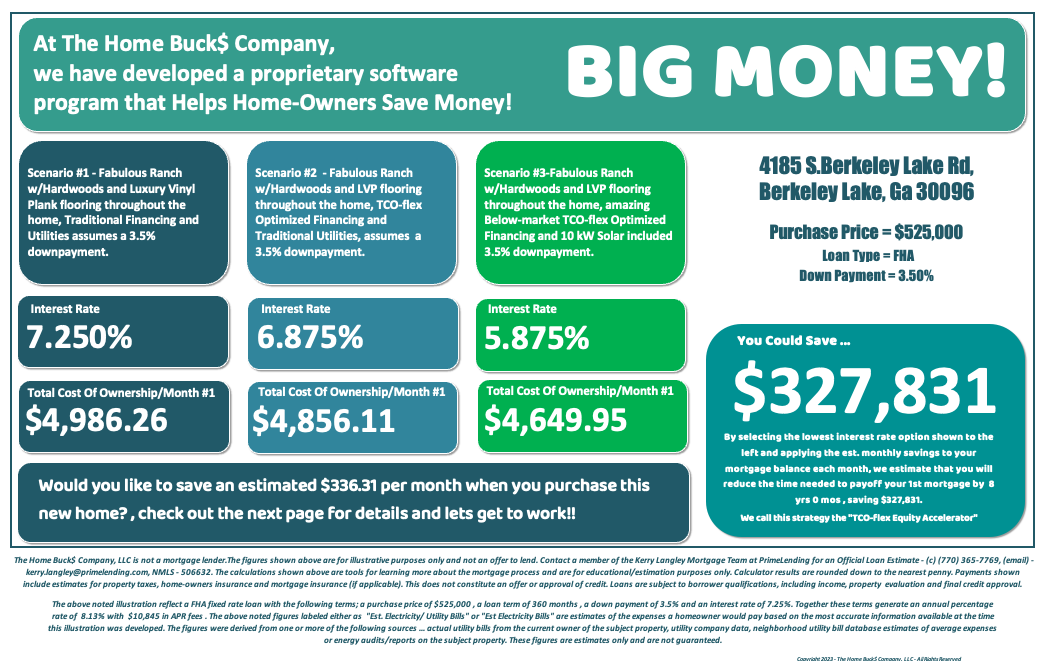

(I call them "DashBoards" ... here is page 1)

(I call them "DashBoards" ... here is page 1)

So what have we done for the potential buyer of this home ...

In Scenario #1, we have shown the prospective buyer the answer to the #1 item they want in a new home ... The Want to Know "Does it fit their initial budget?"(and since the Total Cost of Ownership figures includes an estimate of their mortgage payment and their utility expenses ... we give them a better estimate than any other lender would) and we include that these numbers are based on a loan with a 3.5% down payment.

In Scenario #2, we have shown them that by using the TCO-flex software, we have developed a model where we can drop their permanent interest rate to 6.875% and as a result of doing so, drop the total cost of owning their home $130.15 each month.

In Scenario #3, we have shown the prospective home-buyers that there is still room to save more money. By adding 10kW of Solar into their deal (and financing it with no additional down payment), we can drop their permanent interest rate to 5.875% and as a result of doing so, drop the total cost of owning their home $336.31 the first month they live in their new home. So don't miss this part ... the $336.31 savings is after paying for the solar ... its all included!!

And finally, the last and most impressive two figures on page #1of this dashboard are associated with a repayment strategy we call the "TCO-flex Equity Accelerator"(aka TCO-Accelerator). Simply put, the TCO-Accelerator shows the home buyer how if they apply the monthly savings associated with Scenario #3 to their mortgage each month, they will payoff their mortgage 8 yrs earlier, saving themselves $327,831.

Pretty powerful stuff huh!!

In Scenario #1, we have shown the prospective buyer the answer to the #1 item they want in a new home ... The Want to Know "Does it fit their initial budget?"(and since the Total Cost of Ownership figures includes an estimate of their mortgage payment and their utility expenses ... we give them a better estimate than any other lender would) and we include that these numbers are based on a loan with a 3.5% down payment.

In Scenario #2, we have shown them that by using the TCO-flex software, we have developed a model where we can drop their permanent interest rate to 6.875% and as a result of doing so, drop the total cost of owning their home $130.15 each month.

In Scenario #3, we have shown the prospective home-buyers that there is still room to save more money. By adding 10kW of Solar into their deal (and financing it with no additional down payment), we can drop their permanent interest rate to 5.875% and as a result of doing so, drop the total cost of owning their home $336.31 the first month they live in their new home. So don't miss this part ... the $336.31 savings is after paying for the solar ... its all included!!

And finally, the last and most impressive two figures on page #1of this dashboard are associated with a repayment strategy we call the "TCO-flex Equity Accelerator"(aka TCO-Accelerator). Simply put, the TCO-Accelerator shows the home buyer how if they apply the monthly savings associated with Scenario #3 to their mortgage each month, they will payoff their mortgage 8 yrs earlier, saving themselves $327,831.

Pretty powerful stuff huh!!

So how do you see if the HomeBuck$ program will work for you ... let's talk.

As you may imagine ... my phone rings all day ... the simplest way for us to connect is thru my Calendly Scheduler ... click the link and schedule a time to discuss HomeBuck$...

calendly.com/meetingwithkerry/30-min-call-with-kerry-homebucks

As you may imagine ... my phone rings all day ... the simplest way for us to connect is thru my Calendly Scheduler ... click the link and schedule a time to discuss HomeBuck$...

calendly.com/meetingwithkerry/30-min-call-with-kerry-homebucks